SAP-Embedded Virtual Cards FAQs

The One Essential Resource for Issuers & Customer-Facing Teams

Introduction to This Guide

The following guide will help you address client questions about virtual cards, including SAP’s own embedded virtual card capability.

You’ll learn about the general benefits of virtual cards for buyers and suppliers and how they compare to other payment methods. In addition, you’ll discover more about SAP Taulia’s own virtual card capability — from broad-stroke benefits to implementation details.

One Capability. Two Ways to Pay.

SAP-embedded virtual cards flexes to two different payment options: Pay on Invoice and Pay on PO. This guide features distinct FAQ sections for both to help you understand how they work and their ideal customer profile.

If you have a question that isn’t addressed, please review the additional resources at the end of this guide or contact your organization’s SAP Taulia representative.

1. General Introduction to Virtual Cards

Typically, companies add virtual cards to their mix of payables because they:

- Streamline administration: Virtual cards reduce manual and repetitive payment processes and often consolidate high-frequency, low-value transactions that exacerbate inefficiency during month-end reconciliation.

- Offer robust payment security: 79% of organizations reported they were victims of attempted or actual payment fraud in 2024 (according to an Association of Payment Professionals survey). Virtual cards make fraud much less likely with built-in payment controls.

- Often provide financial incentives: Companies that use virtual cards receive agreed-upon rebates brokered through their bank issuer that help to reduce the cost of goods and services.

- Extend days payable outstanding (DPO): Similar to the credit cards we use daily, companies can hold onto their cash for longer when they acquire supplier goods and services with the credit offered through virtual cards.

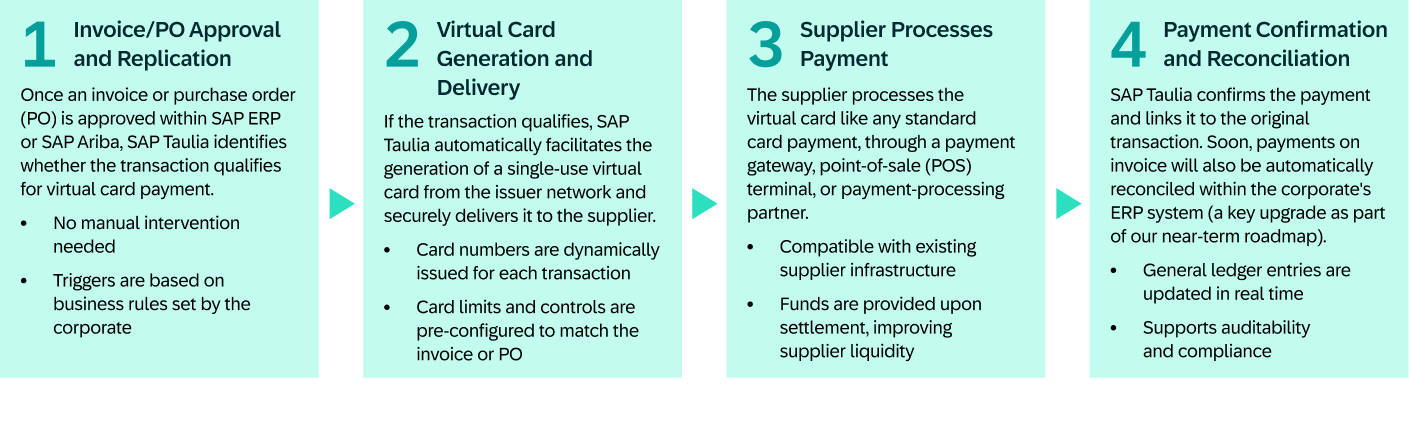

2. SAP Taulia ERP-Embedded Virtual Cards

3. Embedded Virtual Cards in SAP Ariba Buying

4. Go One Step Further: Learn More with Our Dedicated Resources

The information above covers some of the most important topics related to virtual cards. But if you want to find out more, we’ve created the following resources: